TL;DR

- What it is: Lusha’s Q2 2026 B2B Signal Trend Report analyzes live signal data (300M+ verified contacts) from January 1–June 1, 2026 to identify active buying windows across the US, EMEA, and global mid-market.

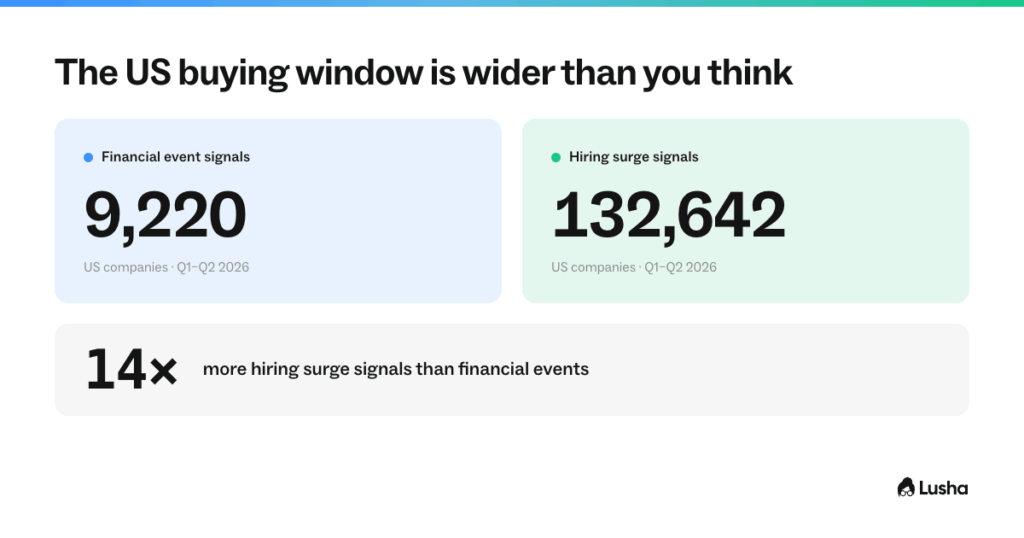

- US market: 132,642 US companies show a hiring surge in Sales, Engineering, or Marketing, while 9,220 have financial event signals (funding, investment, capital activity) — led by Technology, Finance, and Healthcare, with post-funding outreach windows of about 14 days.

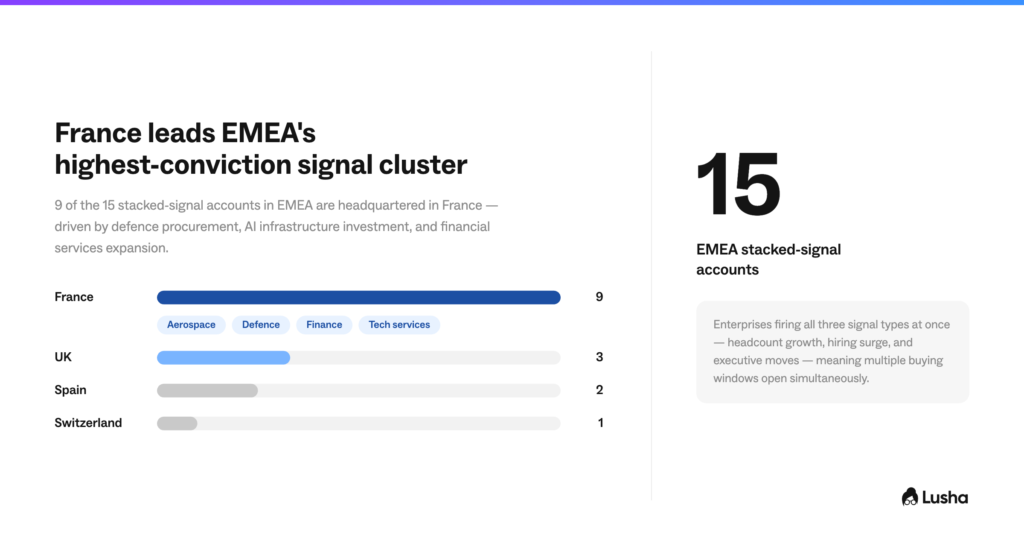

- EMEA market: Over 1.35 million EMEA companies show active growth signals, and 15 major European enterprises carry all three “stacked” signal types simultaneously — 9 of those 15 are headquartered in France, driven by defence procurement, AI infrastructure investment, and financial services expansion.

- Global mid-market: 1,172 mid-market companies (201–1,000 employees) worldwide show financial event signals, concentrated in AI-native software, digital health/biotech, and Asian FinTech, with the tightest response window (7–14 days) of any segment in the report.

Published: June 2026

Data source: Lusha live signal database — 300M+ verified contacts, signals pulled June 1, 2026

Signal window: January 1 – June 1, 2026

Methodology note: Signal counts reflect companies with at least one qualifying event detected in Lusha’s database during the reporting window. Totals represent the active signal universe, not a statistical sample. Industry and geographic breakdowns are based on Lusha company classifications.

Executive summary

Three patterns are running simultaneously across US, EMEA, and global markets in Q2 2026.

01. In the US, hiring surges are the dominant signal — 132,642 companies are actively growing headcount across Sales, Engineering, and Marketing, while 9,220 companies have financial event signals indicating funding, strategic investment, or capital deployment. Technology, Finance, and Healthcare lead both signal types. The ratio — 14 hiring surge signals for every financial event signal — tells outbound teams something important: the buying window in the US is broader than post-funding outreach alone.

02. In EMEA, over 1.35 million companies show active growth signals in Q2 2026. The standout finding: 15 major European enterprises are carrying stacked signals — all three signal types firing simultaneously. These are the highest-conviction accounts in the EMEA landscape right now. France accounts for the majority of them, driven by defence procurement, AI infrastructure investment, and financial services expansion.

03. Globally, the mid-market segment (201–1,000 employees) has 1,172 companies with financial event signals across Technology, Finance, Healthcare, and Business Services. The funding is concentrating in three categories: AI-native software, digital health, and Asian FinTech. These are the fastest-moving buying windows in the global dataset.

The US market: 132,000+ companies in an active buying window

Signal overview

| Signal type | Companies active in Q2 2026 |

|---|---|

| Financial events (funding, investment, capital activity) | 9,220 |

| Hiring surge (Sales, Engineering, or Marketing) | 132,642 |

The 132,642 hiring surge figure is the most actionable number in the US dataset. It means roughly 132,000 companies are currently scaling a function that requires tooling, data, and operational infrastructure to support. Most are in a buying window whether or not they have been contacted.

The financial events pool of 9,220 reflects companies with a detectable capital event — a funding round, strategic investment, or significant financial activity — since January 1, 2026. For outbound teams, this is the time-sensitive pool: post-funding conversations have a 14-day window before budget allocations close and the evaluation process formalises.

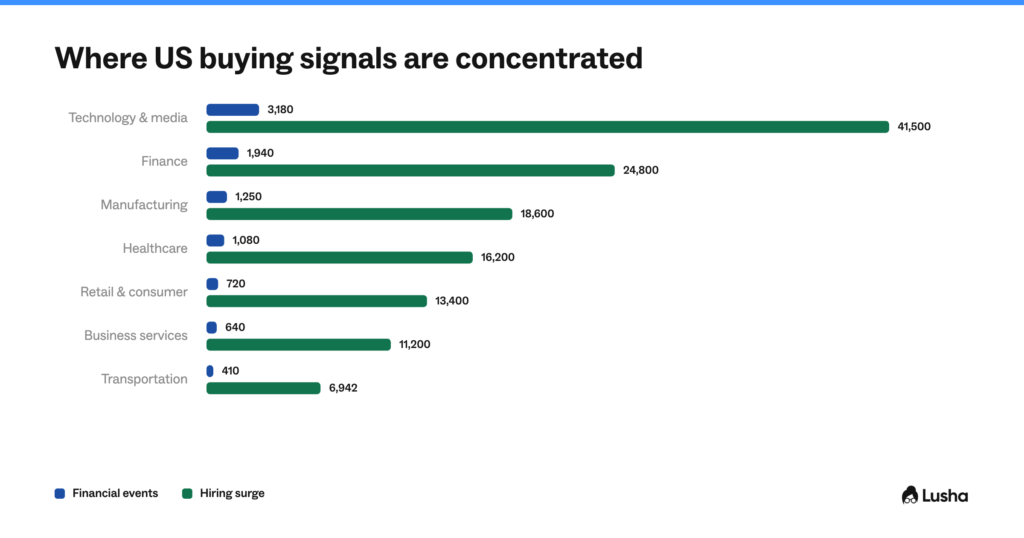

Industry breakdown: financial events

Financial event signals in the US are distributed across every major sector. The four highest-density industries in Q2 2026:

Technology, Information & Media is the most active sector by financial event volume. Software development, IT services, cloud infrastructure, internet platforms, and telecommunications are all showing capital activity. This sector generates more financial event signals per company than any other in the US dataset — and has the shortest time-to-procurement cycle after a funding event.

Finance is the second-densest sector — banking, investment management, capital markets, and insurance are all carrying financial event signals. The signal type in financial services tends to be strategic investment and capital deployment rather than venture funding, which changes the outreach angle. These organisations are deploying into infrastructure, compliance, and workflow tooling.

Healthcare shows sustained financial event activity across hospitals and clinic networks, medical equipment, and biotechnology research. Healthcare financial signals typically precede significant technology and operational procurement cycles of 60–90 days.

Manufacturing — particularly aerospace and defence, semiconductors, pharmaceuticals, and automotive — shows consistent capital activity. The manufacturing sector’s technology spend continues to grow as AI-driven operations and automation displace manual processes.

Industry breakdown: hiring surge

The hiring surge universe of 132,642 companies spans every US sector. Four patterns stand out:

Technology leads by a significant margin. Software development, IT services, cloud infrastructure, and internet platforms are growing Sales, Engineering, and Marketing functions simultaneously. When a technology company surges in all three functions at once, it signals a go-to-market expansion — which means procurement for the tools that support that expansion is happening in parallel.

Financial services is scaling technology and sales capacity. Banking, investment management, and financial services are hiring into Technology and Sales functions at a rate that indicates a digital transformation cycle. This is vendor evaluation territory.

Professional services is growing delivery capacity. Business consulting, outsourcing, HR services, and staffing firms are surging — which drives demand for data, workflow automation, and HR technology.

Retail and consumer are scaling marketing and operations. The retail hiring surge is concentrated in Marketing and Operations rather than Sales, which points to campaign tooling, CRM, and analytics procurement rather than outbound stack decisions.

The US opportunity: the intersection

The highest-priority US accounts are companies carrying both signal types — financial events AND hiring surges. These organisations are simultaneously receiving capital and scaling headcount. That combination puts them in a vendor evaluation window across every function they are growing.

For outbound teams: filter the hiring surge universe by ICP criteria (size, sub-industry, specific function) and cross-reference against companies with financial events. The intersection is the priority call list. The hiring surge alone is a 30-day window. A hiring surge plus a financial event compresses that to 14 days.

EMEA: France leads the highest-conviction signal cluster in Europe

Signal overview

| Signal type | Companies active in Q2 2026 |

|---|---|

| Headcount growth (3-month) | Significant volume across all major European markets |

| Hiring surge | Active across manufacturing, finance, and technology sectors |

| People news (exec hires, departures, promotions) | Most concentrated in UK, France, Germany, and Spain |

| Companies carrying all three signal types (stacked) | 15 |

The 15 stacked-signal accounts are the headline finding from EMEA. These are enterprises showing headcount growth, an active hiring surge, and executive-level people movement simultaneously. That combination means multiple buying windows are open at the same account at the same time.

Geographic breakdown: the France signal

France accounts for 9 of the 15 stacked-signal EMEA accounts — 60% of the highest-conviction enterprise targets in Europe are headquartered in France in Q2 2026.

This is not random. Three converging forces are driving French signal density:

Defence and aerospace procurement. European defence budgets have been increasing since 2022 and the pace accelerated in 2025–2026. French aerospace and defence companies — manufacturers of aircraft, rail infrastructure, satellite systems, and defence electronics — are in an active hiring and investment cycle. Headcount is growing, executive hires are being made, and procurement decisions across their supply chains are being made now.

AI infrastructure investment. France has made AI infrastructure a national strategic priority. Major French technology services firms and industrial manufacturers are investing in AI-driven operations, which is driving both headcount growth (AI engineering and data science roles) and executive movement (new CDOs, CTOs, Chief AI Officers).

Financial services expansion. French banking and financial services institutions are scaling both domestically and in international markets. The people movement signal in French financial services reflects leadership hiring at the VP and C-suite level — these are the contacts who initiate vendor evaluations.

Geographic breakdown: UK, Germany, Spain, Switzerland

UK contributes 3 stacked-signal accounts — financial services (banking) and retail. The UK accounts are notable for the combination of headcount growth and executive movement, which points to leadership transitions at scale.

Germany shows strong headcount growth and hiring surge signals across manufacturing and financial services, but lower people news signal — German enterprises tend to have lower executive turnover than UK and French counterparts, which means the people signal fires less frequently but is more significant when it does.

Spain contributes 2 stacked-signal accounts — in telecommunications and banking. Both are expanding into international markets, which drives the headcount and people signals simultaneously.

Switzerland contributes 1 stacked-signal account — in consumer goods manufacturing — with strong headcount growth and hiring surge signals driven by post-pandemic operational scaling.

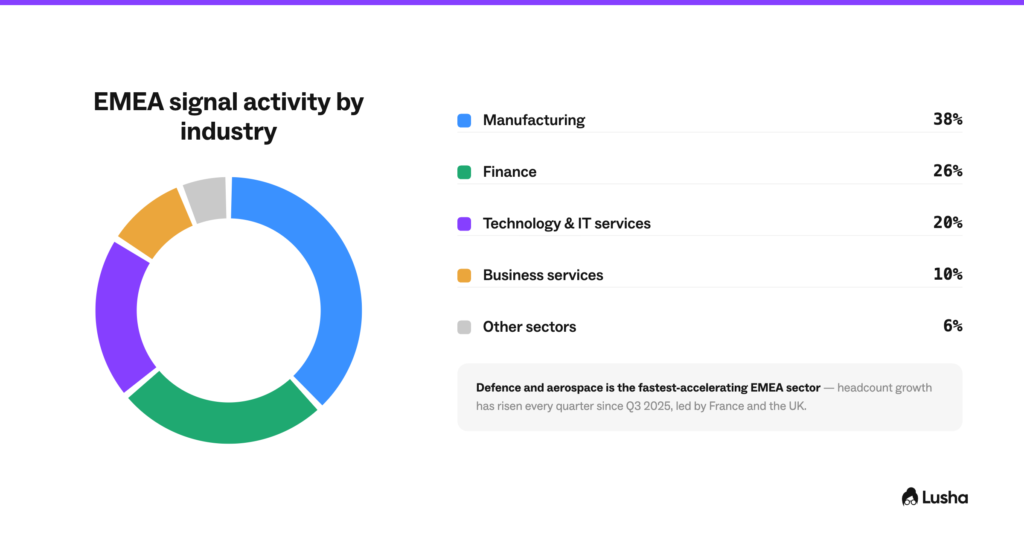

EMEA industry patterns

Four industries dominate the EMEA signal landscape in Q2 2026:

Manufacturing is the largest signal sector by company count. Aerospace, defence, automotive, industrial equipment, pharmaceuticals, and consumer goods all show active signals. The European manufacturing sector is in an investment cycle driven by defence spending, energy transition, and AI-driven automation. Procurement cycles in manufacturing are long but the vendor evaluation window — when the right contact is making tool decisions — opens immediately after a headcount surge or exec hire signal.

Finance is growing technology and compliance capacity. European banking and financial services is hiring heavily into Technology and Compliance functions. The AI and regulatory compliance spend cycle is driving this — new regulations (AI Act, updated AML frameworks) and competitive pressure from FinTechs are forcing traditional financial institutions to upgrade their data and workflow infrastructure.

Technology and IT services are in a delivery expansion cycle. Large IT services organisations headquartered in France and Ireland are scaling delivery capacity to support enterprise AI transformation mandates from their clients. When an IT services firm surges its headcount, the downstream effect is procurement across every tool category they use to deliver services.

Defence and aerospace is the fastest-accelerating EMEA sector. The headcount growth signal in this sector has been increasing quarter on quarter since Q3 2025. European defence budget increases are translating directly into headcount growth and supply chain procurement cycles. Outreach into defence and aerospace accounts in France and the UK has the broadest procurement mandate of any EMEA sector right now.

The EMEA outbound opportunity

For enterprise outbound: The 15 stacked-signal accounts are the starting point. These organisations have multiple buying windows open simultaneously — headcount growth opens a capacity conversation, the hiring surge opens a tooling conversation, and executive movement opens a relationship conversation. Three different contacts at the same account, three different conversation angles, all in the same week.

For mid-market outbound in France: The French manufacturing, defence, and technology services sectors are in the most active expansion phase in EMEA. VP-level contacts in Sales, Technology, and Operations at 200–1,000 employee French companies are in active evaluation mode.

One compliance note for EMEA outreach: All 15 stacked-signal accounts and the majority of the EMEA signal pool are headquartered in GDPR jurisdictions. Outreach data used for EMEA prospecting must come from a provider with independently audited GDPR certification. Lusha holds GDPR certification validated by independent third-party auditors, ISO 27701 accreditation (the highest international privacy standard, accredited by ANAB), and ISO 31700 — not self-declared compliance.

Global mid-market: where the funding is going and why it moves fast

Signal overview

| Segment | Companies with financial events, Q2 2026 |

|---|---|

| Global mid-market (201–1,000 employees), Technology / Finance / Healthcare / Business Services | 1,172 |

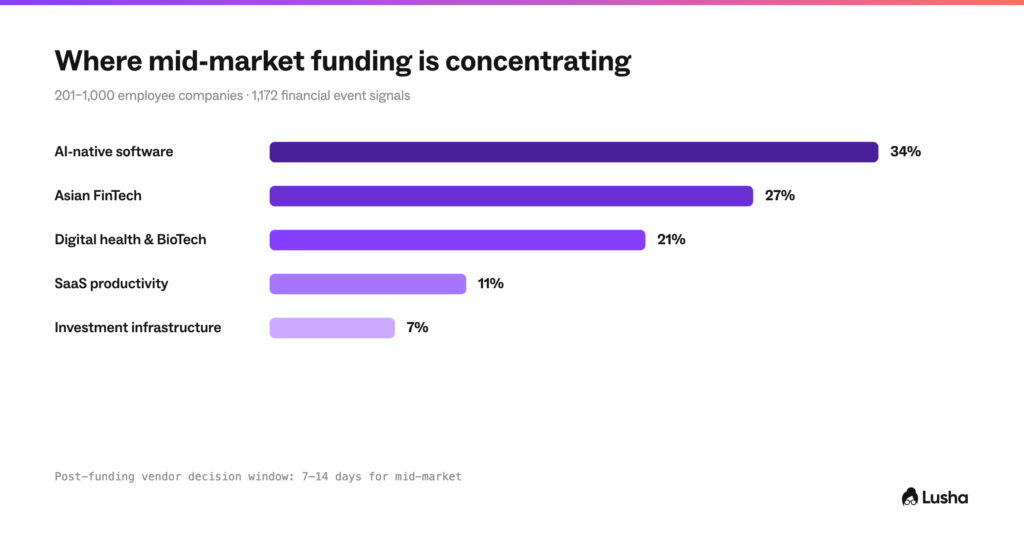

The 1,172 mid-market companies with financial event signals are in the most time-sensitive position of any segment in this report. These organisations are large enough to have real procurement cycles and small enough that a founder, CEO, or VP can make a vendor decision in weeks rather than quarters.

Where the funding is going: three dominant categories

AI-native software is the most represented funding category in the global mid-market pool. AI legal platforms, conversational AI, AI contract management, and GTM data tools are all showing financial event signals in Q2 2026. These are post-funding deployment companies — they have closed a round and are actively building their GTM stack. The vendor evaluation window for supporting infrastructure (data, CRM, enrichment, engagement tools) is open right now, and it closes fast.

Digital health and BioTech — digital therapeutics, wearable health platforms, oncology biotech, and specialist research organisations — all show financial event signals in Q2 2026. Healthcare IT and digital health funding has not slowed from 2025 levels. The procurement cycle after a health tech funding event is typically 30–60 days for tooling decisions, driven by the need to build commercial infrastructure before the product reaches market.

FinTech, particularly in Asia — Indian and Southeast Asian FinTech companies dominate the mid-market financial event pool. India specifically shows the highest concentration of mid-market FinTech funding signals outside the US. Indian FinTech companies are scaling commercial teams, which creates a buying window for CRM, contact data, and sales engagement tooling that mirrors what US SaaS companies were doing in 2018–2020.

Geographic concentration

The mid-market funding signal is global but concentrated in four geographies:

United States is the largest concentration by company count, weighted toward AI software, HealthTech, and FinTech based in San Francisco, New York, and Austin. US mid-market funded companies tend to move fastest on vendor decisions — 14-day post-funding window is the norm.

India is the fastest-growing mid-market signal pool outside the US. Bengaluru and Mumbai are the primary hubs. FinTech, IT services, and digital infrastructure dominate. The signal pool is large and the procurement cycles are slightly longer than the US — 21–30 days post-funding is more typical.

Singapore and the UAE are emerging as mid-market signal hubs. VC firms and FinTech platforms headquartered in Singapore and Abu Dhabi are showing financial event signals. The Gulf and Southeast Asia FinTech corridors are actively deploying capital.

Europe contributes a smaller share of the mid-market funding pool than the US and Asia, but the accounts present are high quality — gaming companies (Finland), development banks (Netherlands), and specialist technology platforms.

The global mid-market opportunity

This is the most time-sensitive segment in the report. The post-funding window for vendor conversations at mid-market companies is 14–30 days. After that, budget allocations are set, the new headcount has been hired, and the evaluation process either has a vendor in it or has closed without one.

The AI software category is particularly acute. AI-native companies that have just closed a round are building their entire commercial infrastructure from scratch — they need a CRM, a data provider, a contact database, and an engagement platform simultaneously. The vendor who reaches a newly-funded AI company in the first two weeks of a round close frequently wins the category before a formal evaluation begins.

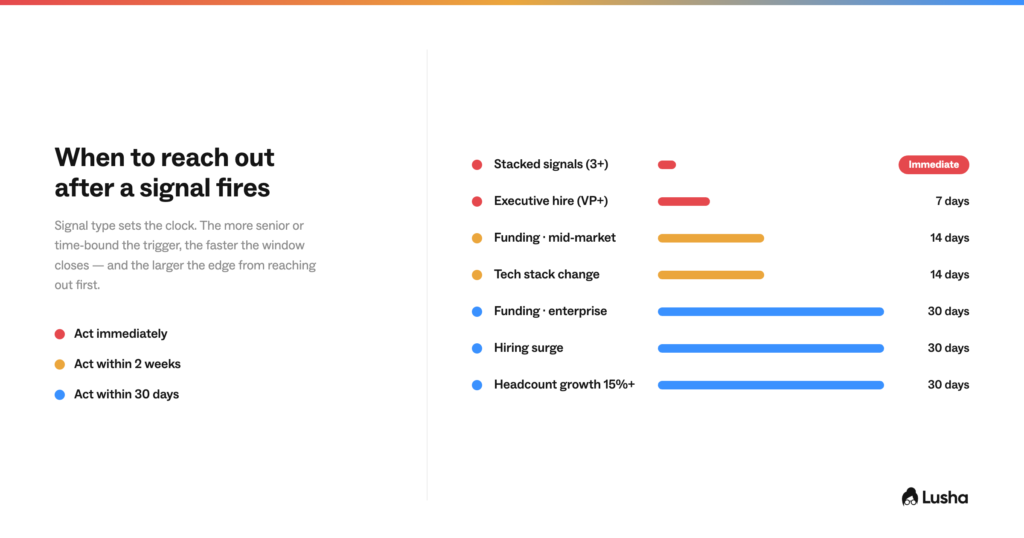

When to reach out: response windows by signal type

Signal response windows

| Signal type | Response window | Outreach angle |

|---|---|---|

| Funding event — mid-market (201–1,000 employees) | 7–14 days | Reference the round, connect to the scaling challenge it implies |

| Funding event — enterprise (1,000+ employees) | 14–30 days | Connect to the deployment mandate the funding creates |

| Hiring surge in target function | 14–30 days | Operational challenge of scaling that function |

| Executive hire (VP/C-suite) | 7 days | Acknowledge the new role directly; position as helping the new leader understand the landscape |

| Headcount growth 15%+ (3-month) | 30 days | Scale conversation — tools, data, infrastructure |

| Stacked signals (3+ types) | Immediate | Multiple entry points open simultaneously — lead with the signal most senior in the org |

The stacked signal priority

The 15 EMEA stacked-signal accounts represent a specific situation: three buying windows are open at the same time. The right approach is not a single outreach to a single contact. It is mapping the buying group, finding the right contact for each signal angle, and running three parallel conversations simultaneously — headcount growth to the COO or Head of Operations, hiring surge to the VP of the surging function, people news to the new executive directly.

This is where buying group mapping matters most. A stacked-signal account with a single-threaded outreach misses two thirds of the open windows.

The mid-market funding window

The 1,172 global mid-market companies with financial events are the most time-sensitive targets in this report. Unlike enterprise accounts where a funding event precedes a 6-month procurement cycle, mid-market companies make tool decisions fast. An AI software company that just closed a $40M round is hiring its GTM team, choosing its CRM, selecting its data provider, and building its outreach stack in the same 4–6 week window. The window is narrow and the decision is happening whether or not a vendor has reached out.

Why signal type determines response time

The response window difference between executive hires (7 days) and headcount growth (30 days) is not arbitrary. An executive hire opens a window immediately because the new leader is evaluating the existing stack in the first weeks — before they have made any commitments. After 30 days, the new leader has either started an evaluation process (where you should already be in it) or decided to keep the current stack. The window closes when a decision is made, not when a calendar date passes.

Funding events at the mid-market level close faster than at enterprise because mid-market companies have fewer procurement layers. A VP at a 500-person funded company can approve a tool purchase in a week. A VP at a 50,000-person enterprise needs three approvals and a security review.

What sales and revenue teams should do with this data

For teams targeting US enterprise

The hiring surge universe of 132,000+ US companies is large enough to be filtered and prioritised. The right approach is not to work the entire list — it is to intersect the hiring surge pool with financial event signals and ICP criteria (industry, size, specific function surging) to produce a priority subset. That subset is the call list for the next 30 days.

The US market in Q2 2026 is a volume environment. The signal pool is large, the windows are real, and the competition for attention in the priority accounts is high. Signal-based outreach that references the specific trigger — “your Sales team has grown significantly in the last 90 days” — converts at a materially higher rate than ICP-filtered cold outreach because it is demonstrably relevant at the moment it arrives.

For teams targeting EMEA enterprise

The EMEA market in Q2 2026 rewards precision over volume. The 15 stacked-signal accounts are a narrow, high-value list. The right approach is to map the buying group at each account, find verified contacts across all three relevant functions, and run coordinated outreach that connects each signal to a specific business challenge.

France is the highest-signal market in EMEA right now. Teams that do not have coverage of the French enterprise market are missing the most active procurement cycle in European B2B in 2026. The defence, aerospace, and technology services sectors in France are in simultaneous expansion — headcount is growing, leaders are being hired, and vendors are being evaluated.

For teams targeting global mid-market

Speed is the differentiating factor. The mid-market window is 14 days for funded AI software and FinTech companies. Being the second vendor to reach a newly-funded 500-person AI company is significantly less valuable than being the first. The companies in the financial event pool right now will have made most of their tooling decisions within the next 30 days.

The Indian FinTech cluster is the most overlooked opportunity in this dataset. Large pools of mid-market FinTech companies showing financial event signals in Bengaluru and Mumbai are in the early stages of building commercial infrastructure that US and European SaaS companies have been building for a decade. The vendor decisions being made in Indian FinTech right now are foundational — the winners of those decisions will have long-term embedded relationships.

Methodology and data notes

Data source: Lusha’s live signal database, queried June 1, 2026. All signal counts reflect companies with at least one qualifying event detected between January 1 and June 1, 2026.

Signal definitions:

- Financial events: funding rounds, strategic investments, capital activity, IPO signals, and significant financial announcements

- Hiring surge: company showing significant open role growth in one or more functions versus the prior 30/60/90-day baseline

- Headcount growth (3m): verified headcount has grown on a 3-month comparison basis

- People news: executive hires, departures, promotions, and leadership changes at VP level and above

- Stacked signals: company showing 3 or more distinct signal types simultaneously in the same reporting window

Geographic classification: Based on company headquarters as recorded in Lusha’s database.

Industry classification: Lusha’s proprietary taxonomy. “Technology, Information & Media” includes software, IT services, telecommunications, internet, and media companies. “Manufacturing” includes pharmaceuticals, aerospace, defence, automotive, and industrial equipment.

Company-level data: This report presents aggregate trends and signal volumes. Individual company names are not disclosed. Signal data is used to identify market patterns, not to make claims about specific organisations.

Compliance: All data accessed through the Lusha connector for Claude under Lusha’s certified compliance framework: GDPR, CCPA, SOC 2 Type II, ISO 27701 (ANAB-accredited), ISO 31700, and TRUSTe. Data is sourced from business-only contacts under legitimate interest provisions applicable to B2B contact data.

Run these queries yourself

Every trend in this report is reproducible as a live Lusha query. Connect Lusha to Claude and ask:

“Find [industry] companies in [geography] with [signal type] signals in the last 30 days, VP-level contacts in [function], verified email and direct dial.”

The data in this report reflects the signal state as of June 1, 2026. Signal windows are time-sensitive — run a live query to get the current state for any specific industry, geography, or company segment.